Sacramento, CA – In a tentative ruling today, the Sacramento Superior Court rejected an insurance industry attack on regulations that limit the amount of advertising costs insurers can pass through to consumers in their premiums. The regulation is part of the landmark Prop 103 insurance reform initiative that has saved California drivers $102 billion since 1988, according to the Consumer Federation of America.

“The court’s ruling upholds the regulation prohibiting insurers from charging consumers higher premiums to cover the costs of all their exorbitant advertising campaigns – including plastering sport venues with their company logo,” stated Pamela Pressley, Consumer Watchdog’s Litigation Director. “The decision properly applies 1st Amendment law and recognizes that the state has a substantial interest in ensuring that insurance rates are not excessive.”

Read the court’s tentative ruling here: http://www.consumerwatchdog.org/resources/tentativerulingmercuryvjones.pdf

Mercury and the Insurance Industry Fall Short In Legal Challenge to Prop 103 Rules Prohibiting Excessive Rates

After a full public hearing requested by Consumer Watchdog, Mercury’s application for an overall 8.8% rate hike on its homeowners insurance line was rejected, and the company was ordered to reduce its overall rates by 5.4%. Mercury then filed suit, arguing that the rate regulations were unconstitutional because they denied the company a fair profit. In a ruling in June 2014, the Superior Court upheld Insurance Commissioner Dave Jones’ order requiring Mercury to lower its overall homeowner’s rates by 5.4%. The Commissioner’s 2013 rate decrease order saved Mercury homeowner policyholders over $16 million in annual premiums.

The court also upheld the regulation prohibiting Mercury from passing on to its homeowners policyholders advertising expenses totaling $83 million, including advertising of the “Mercury Insurance Group” logo at the Mercury Open tennis tournament.

Read the court’s June 2014 order here: http://www.consumerwatchdog.org/resources/rulingonpetitionfor_writandcomplaintfordeclaratoryrelief6-14-14.pdf

Six lobbying groups representing virtually all property-casualty insurers selling homeowners and auto insurance in California, including State Farm, Farmers, Allstate, Progressive, Liberty Mutual, and Nationwide intervened in the lawsuit, joining Mercury’s attack on the regulations. The lobbying groups also challenged a limit on the kinds of advertising expenses that can be passed through to policyholders, claiming the limit deprived insurance companies of their free speech rights.

The Court’s ruling today decisively rejected the insurance industry’s arguments that limiting the amount of insurance advertising costs they can foist on their customers infringes on their 1st Amendment rights. Following the California Supreme Court’s landmark 1994 decision upholding Prop 103 against constitutional attack in 20th Century Ins. Co. v. Garamendi, the court’s ruling stated:

[T]he government has an interest in ensuring that regulations governing rate setting … recognize the “reasonable cost of providing insurance.

…[A]lthough some types of advertising could be excluded under the regulation (such as event sponsorship unrelated to a specific insurer), this potential exclusion does not render [the regulation] more extensive than necessary to serve the government’s interest in ensuring that insurance rates are neither excessive nor inadequate.

Proposition 103 and the Prior Approval Rate Regulations

Proposition 103, approved by voters despite an $80 million industry campaign, requires auto, home and business insurance companies to open their books to public scrutiny and justify rate changes before they take effect. The California Supreme Court unanimously upheld the law and the rate review regulations in 1989 and 1994, respectively. According to a November, 2013, report by the Consumer Federation of America, the Proposition 103 prior approval regulations have saved California motorists $102 billion since the measure passed in 1988 – approximately $8000 for every family in California. California’s average auto insurance premium was lower in 2010 than in 1989, the report found – the only state in the nation where premiums went down. Read the CFA report here: http://www.consumerwatchdog.org/blog/100-billion-win

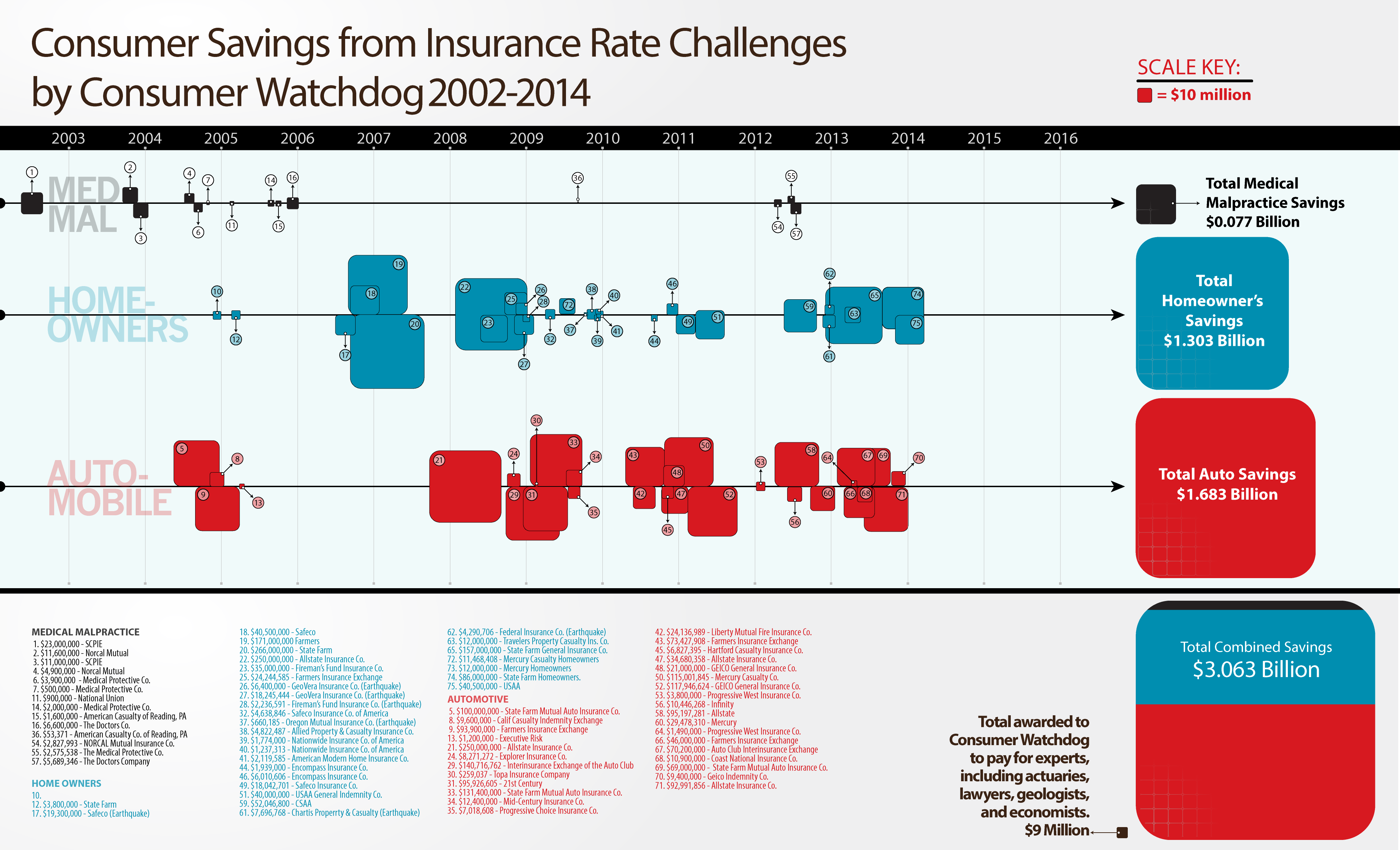

Challenges brought by Consumer Watchdog to proposed insurance rate hikes that were found to be excessive have saved consumers over $3 billion over the last decade: http://www.consumerwatchdog.org/sites/default/files/images/RateSavingsChart.png

– 30 –

{kind=link}