California is the single biggest market for insurance in the nation. Between 1985 and 1987, insurance premiums in California rose dramatically. In 1986 alone, automobile premiums in California increased by 22%, while the consumer price index increased 3.1%. The increases led to public outrage.1

During 1987, California consumer advocacy groups sponsored legislation that would have instituted limited regulation of property-casualty insurance premiums, including auto insurance, and repeal of the industry's exemption from state antitrust laws.

The insurance industry's political prowess in state capitals is legendary, however. And in California, insurance companies spent lavishly to protect their profits against reform. According to disclosure reports submitted by insurers and other lobbying associations to the California Secretary of State and the California Fair Political Practices Commission, the insurance industry spent over $108 million on lobbying expenses in California alone between 1983 and 1996. This figure does not even include campaign contributions!2

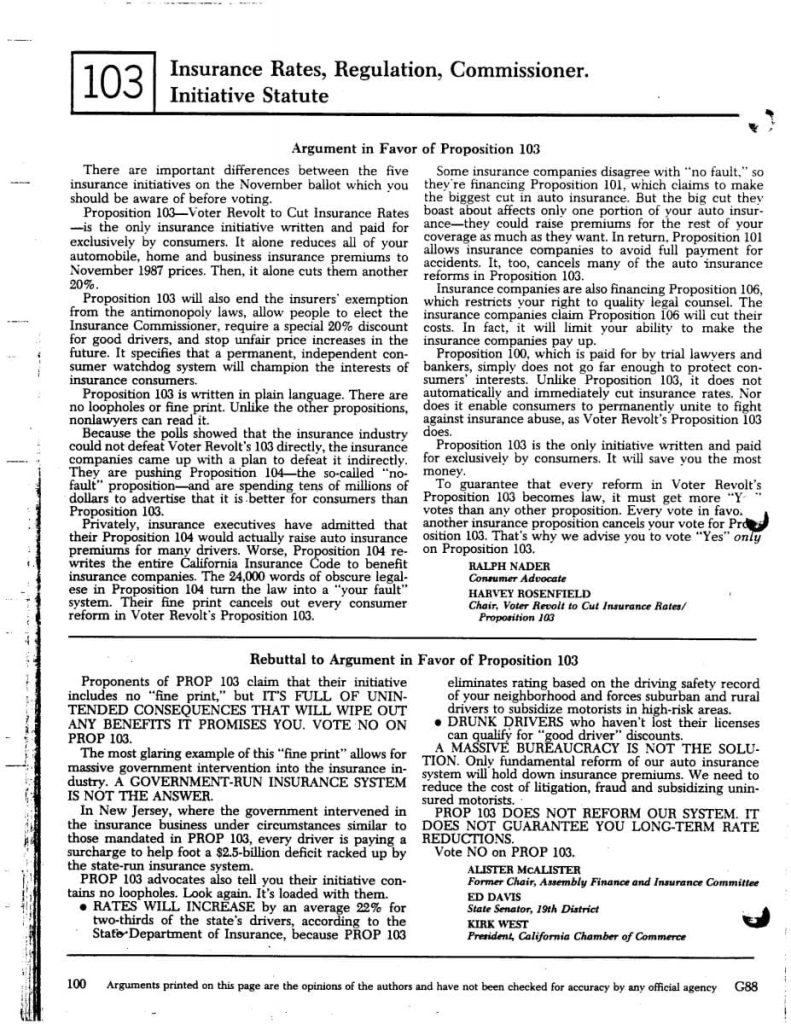

Here are the original arguments in favor of and against Proposition 103 published by the Secretary of State prior to the 1988 election.

Here are the original arguments in favor of and against Proposition 103 published by the Secretary of State prior to the 1988 election.

Not surprisingly, opposition from insurers blocked the passage of the consumer reform legislation in Sacramento. A coalition of citizen groups — led by FTCR President Harvey Rosenfield — decided to draft a ballot proposition. "The Insurance Rate Reduction and Reform Act of 1988" was placed before California voters on November 8, 1988.

The initiative, which was qualified for the ballot as Proposition 103, addressed the industry's unique financial cycle and its cost-plus nature through a series of short- and long-term reforms designed to improve the insurance marketplace, remedy certain industry practices, and provide greater protection to policyholders.

To the right is a mailer from the insurance industry's unsuccessful $80 million campaign to defeat Prop 103.

To the right is a mailer from the insurance industry's unsuccessful $80 million campaign to defeat Prop 103.

As described in greater detail through the links below, Proposition 103:

- mandated a 20% rollback in automobile, homeowner, business, and all other property-casualty premiums;

- instituted stringent controls on insurance company profiteering, waste, and inefficiency through a regulatory process subject to public scrutiny and participation;

- ended monopolistic insurer practices; required insurers to base auto insurance premiums on driving safety record rather than zip code;

- mandated a 20% good driver discount; and,

- made the Insurance Commissioner an elective post.

Insurance Companies Offer A Trojan Horse

Concerned that it could not defeat Proposition 103, the insurance companies responded by placing three separate measures on the ballot to compete with 103:

- Proposition 101, sponsored by Coastal Insurance Company, limited payments for pain and suffering in excess of economic damages unless the injured victim met a specific injury threshold.

- Proposition 104 called for the establishment of a no-fault auto insurance system in California modeled upon New York's verbal threshold-based system.

- Proposition 106, also sponsored by insurers, imposed limits on the size of contingency fees a plaintiff could pay to an attorney in any tort case.

With polls indicating overwhelming public support for Proposition 103, the insurance industry recognized that the measure would be difficult to defeat. So they employed a "Trojan Horse" strategy unique to California's initiative process. Included within Proposition 104's text were provisions conflicting with each reform provision of Proposition 103.

Article II, section 10(b) of the California Constitution provides that, in the event that two measures with conflicting provisions are approved by the voters, the provisions of the initiative that obtained the greater number of voters prevail. The insurers hoped to invalidate 103 by getting more votes for Proposition 104, a strategy that was revealed to voters by the official state ballot pamphlet. It noted that Proposition 104: "[c]ancels Prop. 100, 101, 103. Restricts future insurance regulation legislation."

The presence of three insurance industry ballot measures — all targeting lawyers who represent consumers — provoked a response from the California Trial Lawyers Association and some other advocacy groups. They sponsored Proposition 100, a far less comprehensive version of Proposition 103; unlike 103, Proposition 100 contained language canceling out Propositions 101, 104 and 106.

Never before in California — or since — have there been five competing measures on a single ballot. But this was not the only record broken in the 1988 insurance wars.

An $80 Million David vs. Goliath Battle

In their campaign to defeat Proposition 103, insurers spent over sixty million dollars. The CTLA organization spent $16 million. Conventional wisdom dictated that Proposition 103, with no money for advertising, didn't have a chance.3

To promote Proposition 103, Rosenfield created a campaign organization which Ralph Nader aptly named "Voter Revolt." Rosenfield hired political consultants, including signature-gatherers and direct mail experts, to get the measure on the ballot and raise money. By November, the campaign had spent $2.9 million, the vast majority of which went to pay for mailings to voters, asking them to sign petitions and make donations averaging less than $10 each.

On election day, the organization was deeply in debt. But the enormous amount of advertising by the insurance industry had back-fired. The industry's unprecedented level of spending had drawn enormous attention from the public and the news media. Ralph Nader's active campaigning for the measure across the state helped cut through the confusion generated by the insurance industry's ad campaign.4 The battle became that of David v. Goliath.

On Election Day, in a stunning upset, the insurance industry was vanquished. Only Proposition 103 was approved, by 51% of the voters.

Footnote References:

1. National Ins. Consumer Org. (NICO), A Consumer Triumph: Proposition 103 Revisited 19 (1992) (citing National Ass'n of Ins. Comm'rs, supra note 27, 1981-91); California Dep't of Fin., California Statistical Abstract 60 (1996). See, e.g., Scott Armstrong, California Car Insurance Revolt: Soaring Premiums Spark Drive for Reform Initiatives, Christian Sci. Monitor, Feb. 22, 1988, at 3; Sam Richards, Groups Target Insurance Rates, Tracy Press, Jan. 19, 1988, at 1.

2. For a look at the insurance industry's political activity nationwide, read Walter L. Updegrave, How the Insurance Industry Collects an Extra $65 Billion a Year from You by . . . Stacking the Deck, MONEY MAG., Aug. 1996, at 50.

3. Kenneth Reich, Insurance Fight Cost Initiative Backers a Total of $83.9 Million, L.A. TIMES, Feb. 7, 1989, at 3. Also: Susan Seager, Insurance Initiative War Hits Record $63.5 Million, L.A. HERALD-EXAMINER, Oct. 29, 1988, at A3. Ramon G. McLeod, Voters Angry About Rates for Auto Insurance, S.F. CHRON., June 10, 1988, at A14.

4. Nader's role in clarifying matters for the voters was later examined by Arthur Lupia in Shortcuts Versus Encyclopedias: Information and Voting Behavior in California Insurance Reform Elections, 88 AM. POL. SCI. REV. 63, 72 (Mar. 1994).