Medical malpractice insurance premiums increased more quickly in states that enacted caps than in states that did nothing.

- A national analysis for Americans for Insurance Reform by Robert Hunter, former Texas Commissioner of Insurance, Federal Insurance Administrator under both Presidents Carter and Ford, and President and Founder of the National Insurance Consumer Organization, comparing malpractice insurance premiums in states that enacted limits on compensation for malpractice victims between 2002 and 2015 finds no correlation between enactment of tort limits and insurance rates. In fact, the reverse happened: Read the AIR Study.

“States that enacted new limits on patients’ legal rights in medical malpractice cases (caps on damages plus other traditional tort reforms) saw an average 22.7 percent decrease in pure premiums from 2002 to the present – but states that did nothing saw a larger average drop of 29.5 percent.”

“States that enacted or lowered caps on non-economic damages saw an average 21.8 percent decrease in pure premiums over the period – but the states that did not saw an even greater average drop of 28.9 percent.”

Rate regulation, not limits on patient compensation, reduced and then stabilized rates in CA.

- California’s system of prior approval rate regulation is the strongest in the nation. It was enacted by California voters in Proposition 103 in 1988. It prevents malpractice insurance companies from raising rates without publicly justifying any increase and getting approval from an elected insurance commissioner. Prop. 103’s regulation, not the cap on damages, lowered doctors’ malpractice premiums in California.

RATE REGULATION: The Rx For Medical Malpractice Insurance Rates

- In the 13 years after the cap was enacted, malpractice insurance premiums spiked 450% in California. Only when Prop. 103 was enacted in 1988 did rates drop 20%, and stabilize.

This graph (published in the Sacramento Bee) compares what happened to malpractice insurance premiums after California’s damage cap law, passed in 1975, and after the passage of insurance reform Proposition 103 in 1988.

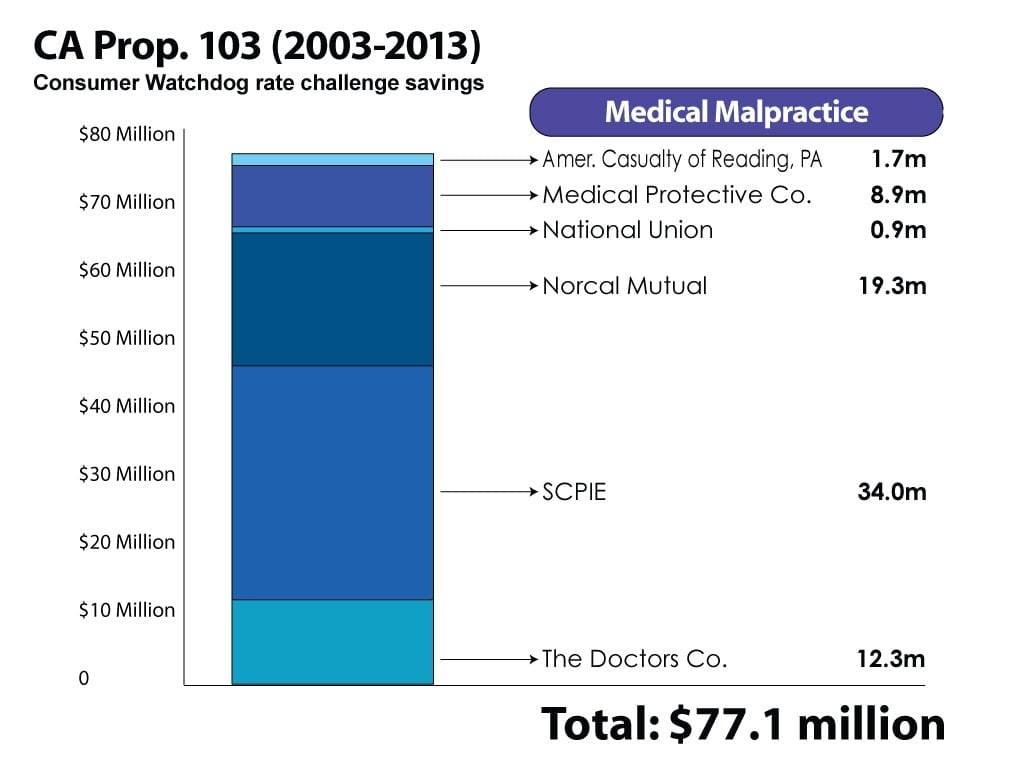

- Public challenges to excessive medical malpractice insurance rates, brought by Consumer Watchdog using Proposition 103’s public participation rules, have saved medical providers $77 million.

Malpractice insurers are raking in the profits in California.

- The financial statements of California’s top six medical malpractice insurance companies show that the companies are very profitable. The top six companiespaid out to patients harmed by medical negligence, on average over the last five years, just 37.4 cents of every premium dollar collected from medical providers.

This means that malpractice insurers had an average 62.6 cents of each premium dollar, plus all investment income, left over for expenses, defense, and profit.

Even after defense costs are added to losses, California’s largest medical malpractice insurance companies spent an average of just 66.7 cents per premium dollar.