Los Angeles, CA— A new report (opens in new tab) by Consumer Watchdog warns that Uber has nearly doubled the size of its self-funded insurance reserves since 2023 with an eye toward funding its robocar rollout should it succeed in plans to limit its liability for auto accidents in California and across the nation. This report was first covered by the LA Times (opens in new tab).

Uber created a captive insurance company, Aleka, run by Uber executives to stockpile $12.5 billion in self-funded insurance reserves as it seeks $10 billion to finance its robotaxi rollout. If Uber succeeds in strictly limiting its liability for auto accidents, through a pending California ballot measure and tort reforms in New York, Indiana, and Nevada, the company can reclassify the reserves as unrestricted cash to finance its robocars with significant tax advantages, the report says.

“Uber’s corporate strategy is clear: limit liability, over-reserve, and re-invest the savings in robocars,” the report states. “Meanwhile innocent accident victims are being asked to give up their rights to recover for their injuries in all auto accidents so Uber and its executives can profit from its cynical strategy.”

“Uber’s investment in a 2026 California ballot measure restricting victims’ medical recovery and access to contingency fee attorneys will allow it to free itself from liability and open up its ‘piggy bank’ of insurance reserves for investing in its rollout of robotaxis. Those robotaxis, freed from full liability for injuries or death, could give Uber a ‘license to kill.’”

The report also shows how Uber’s top policy executive misrepresented the company’s insurance costs and structure to the California legislature in 2025 when securing a reduction in how much uninsured motorists coverage the company must have through SB 371. It documents bonuses paid to top executives to pass SB 371 and other limits on accident victims’ rights.

Read the report: (opens in new tab) “Uber’s License To Kill Insurance Scam: How Uber Is Limiting Its Liability To Raid Its Insurance Reserves & Fund Robotaxis.”

Among the key findings:

- While Uber claims its insurance premiums are excessive, the company self-funds about 95% of its risk, according to public documents. Toward that end, Uber executives formed a captive insurer in Hawaii— Aleka Insurance Inc. Aleka is run by Uber executives and is a wholly-owned Uber subsidiary exclusively handling Uber’s self-insurance. Uber has accumulated $12.46 billion in insurance reserves in 2025, a 27% increase from the $9.8 billion in reserves in 2024, and nearly doubling its $6.7 billion reserves in 2023. By internalizing nearly 95% of its insurance risk, Uber maintains control over premium flows generated from rides, rather than relying on traditional third-party insurers. Since the money is reserved for claims payout, it is not taxed as profits would be. If reclassified as unrestricted cash, the money could be taxed in a year when Uber made a big investment in robotaxis and would have less profit to tax.

- The company’s insurance reserves grew nearly twice as much as trips made by drivers between 2023 and 2025, according to Uber’s own financial statements, indicating that Uber may be over-reserving. Demonstrating how the company considers its insurance reserves fungible, Uber transferred about $4.1 billion from its insurance reserves to cash on its balance sheet, according to its financial disclosures, during 2024 and 2025. (2025 annual report, pg. 122; 2024 annual report, pg. 128).

- Aleka Insurance’s entire board and executive committee are or have been executives at the parent company Uber. Since Aleka is a privately-held, wholly-owned subsidiary, Uber is under no obligation to disclose any information on the company’s finances and can instead fold Aleka’s financials into its own—allowing Uber executives to obfuscate what would otherwise be public information.

- Uber’s top public policy executive misrepresented the company’s insurance structure to the California legislature in 2025 when securing a reduction in its uninsured motorists coverage through SB 371. “In LA County, 45% of every fare is a straight pass-through to government-mandated insurance,” said Ramona Prieto, Uber’s head of public policy. In fact, the company was paying itself for insurance and at a rate that it set and allowed its reserves to grow by nearly 100% from 2023 to 2025. In other words, Uber appears to be overcharging itself for insurance premiums that it claimed was bleeding its riders dry in order to secure a reprieve from a state legislative mandate.

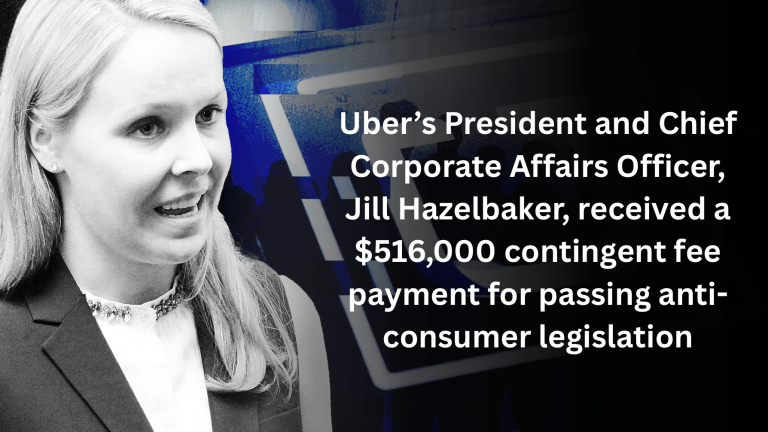

- Unbeknownst to the California legislature, Uber made its executives’ compensation contingent on passing SB 371 and other “insurance reform” efforts in 2025. Uber’s Chief Marketing Officer and SVP of Public Affairs Jill Hazelbaker added $516,000 to her pay and was promoted with a $5 million stock equity grant. Prieto has a “shadow” executive bonus strategy not disclosed to shareholders. Her fiancé Juan Rodriguez is a principal in the campaign consulting firm Bearstar and the media buying firm Polaris, which were paid a total of $9.2 million, thus far, in 2026 for consulting and advertising related to Uber’s ballot measure to limit liability for accident victims.

- Uber’s record with robotaxis is disastrous, as outlined in Consumer Watchdog’s previous report “A License To Kill: How Uber’s Rush To Close Courthouse Doors And Roll Out Robocars Threatens Public Safety.” Uber’s robocar rollout in Arizona was the first and only known instance of a robocar killing a human being. Uber has failed to test its robocars to the degree that Waymo has, and its cars are more cheaply made with fewer sensors.

“There can be no more dangerous a situation than giving a company whose philosophy is ‘move fast and break things’ the keys to $10 billion worth of robocars with little liability or legal accountability attached for the injuries they cause,” the report states.

“Uber is building a financial war chest at the same time as it is minimizing its obligations to the very people harmed by its operations,” said Justin Kloczko, the Tech Director at Consumer Watchdog and author of the report. “Funds intended to compensate crash victims could instead be redirected to bankroll a risky automation agenda. If successful, this strategy could allow the company to deploy autonomous vehicles with reduced liability, effectively granting a license to kill.”