If the goal of Insurance Commissioner Ricardo Lara’s new intervenor compensation regulations is to bring in new intervenors into the process, his regulations will do the opposite. By making it harder for intervenors to be paid, he will discourage intervenors from participating.

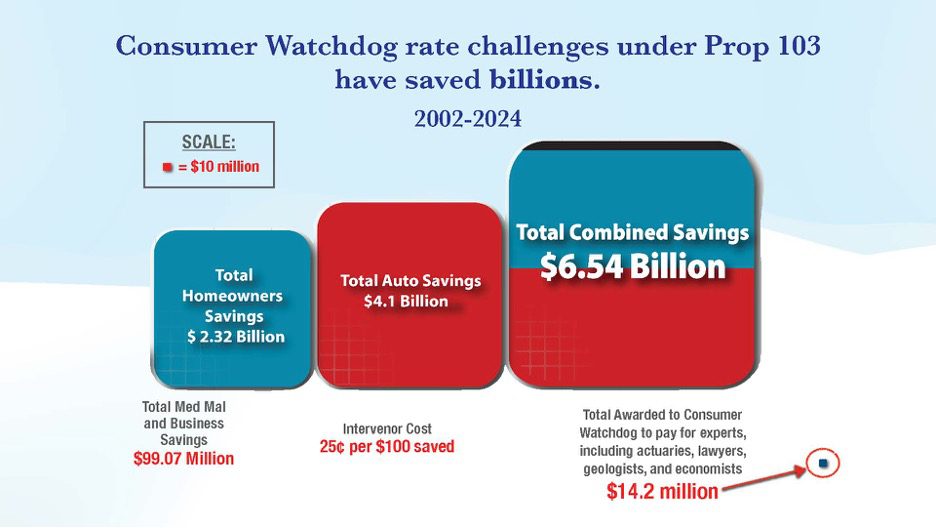

First, Lara fails to acknowledge the value of the intervenor process. Consumer Watchdog’s interventions from 2002 – 2024 have saved consumers $6.4 billion on their insurance bills. The total awarded to Consumer Watchdog to pay for experts, including actuaries, lawyers, geologists and economists in those challenges was $14.2 million. The intervenor cost is 25 cents for every $100 saved.

Lara’s hostility may come from the fact that Lara’s Department of Insurance seems to want companies to get hikes whether they deserve them or not. Lara approved 97% of the rate increase requested in rate filings from January 2022 to October 2023 without public intervenor participation. When Consumer Watchdog participated as an intervenor, the percentage of the rate increase approved in homeowner insurance cases was 62% and in auto insurance cases it was 71%.

Moreover, the time until rates were approved in cases with intervenors and without intervenors’ public participation is nearly identical. Intervenors are not causing delays.

Last year alone Consumer Watchdog’s interventions saved over $1 billion in rate hikes.

Lara has no reason to change the intervenor compensation standard except to get insurance companies unjustified rate hikes quicker and as revenge against his critics.

By changing the definitions of “substantial contribution” and “reasonableness,” Lara is essentially stating that if “I don’t agree with you, you don’t get paid.” (The yellow underlined is the addition.)

“Substantial Contribution” means that the intervenor substantially contributed, as a whole, to a decision, order, regulation, or other action of the Commissioner by presenting relevant issues, evidence, or arguments which were separate and distinct from those emphasized by the Department of Insurance staff or any other party, such that the intervenor’s participation makes a significant, distinct contribution to the Commissioner’s adoption of a decision, order, or regulation, and resulted in more relevant, credible, and non-frivolous information being available for the Commissioner to make the Commissioner’s decision than would have been available to a Commissioner had the intervenor not participated. A substantial contribution may be demonstrated without regard to whether a petition for hearing is granted or denied.

It’s like a loser pays legal provision, except Lara is judge and jury. The regulations remove the power of the Administrative Law Judges (ALJ) over the process, completing a coup that Lara accomplished with the removal of ALJ Kristin Rosi last year and his office taking over intervenor compensation decisions from the ALJs at the same time. With Lara in office, you can bet the insurers will win and the public will lose. Providing credible information that was separate from what the Department presented and reduced a rate informally or allowed for an enlightened decision used to be enough.

In the State Farm proceeding held in the Spring, for example, our presence and information resulted in the company reducing its original interim rate request from $914 million to $748 million — saving policyholders $166 million. The Department of Insurance staff signed off on the interim request. If we had not challenged the company, it would have gotten its full rate hike. However, since we argued State Farm had not justified the rate hike, and the Commissioner granted it, our participation could go uncompensated under these new rules.

The point of the intervenor system is to have a counterbalance to the insurance industry and their legions of attorneys, experts and actuaries. That’s why the current regulations require insurers to disclose their rates/fees/costs if they object to an intervenor’s. Lara redlined that provision in his draft regulations.

g) Any party questioning the market rate or reasonableness of any amount set forth in the request shall, at the time of questioning the market rate or reasonableness of that amount, provide a statement setting forth the fees, rates, and costs it expects to expend in the proceeding.

The draft regulations also limit the number of intervenor experts and attorneys while insurance companies can hire as many as they like and, under the regulations, hide the cost from the public and the decisionmaker.

Excessive. Services are excessive when..The overall number of persons staffed in a proceeding shall be deemed reasonable if there are no more than five persons staffed in that proceeding, consisting of (A) no more than one administrative support staff member responsible for clerical tasks, (B) no more than two staff members performing substantive work such as research, drafting, and analysis, (C) no more than one subject matter expert providing technical expertise essential to the proceeding, and (D) no more than one supervising staff person providing oversight, strategic direction, and final review.

Then there are a host of other procedural hurdles designed to stop compensation for public participation, such as injecting “duplicative” and “cumulative” standards into a new “reasonableness” standard. These are hooks for the Commissioner to deny compensation if an argument is similar to one made by a Department actuary or made in more than one proceeding.

And there is the new vexatious standard that basically prevents an intervenor for pushing for new information from insurance companies that can disprove the need for a rate hike, and prevents recommendations that disagree with a proposed regulation from being compensable.

3) Vexatious. Services are vexatious when they (A) relate to the use of procedural motions as a means of obstruction rather than to address genuine concerns, (B) relate to oppositional efforts that do not lead to alternative fact-based recommendations or that do not provide meaningful critiques that could improve a regulatory outcome, (C) involve lengthy or unfocused presentations that do not engage with the specific issues under consideration, (D) present materials or arguments that are not relevant to a proceeding, or (E) are engaged to seek information beyond what is reasonably necessary to the disposition of a proceeding.

Intervenors would be between a rock and a hard place. If we seek information beyond what the Department thinks is reasonably necessary that’s vexatious and not compensable, but if we duplicate the information the Department seeks then that’s duplicative and not compensable.

The way the process works our actuaries run numbers based on the prior approval formula to find a rate indication, which often differs from the Department and the companies. We then seek more information to prove or disprove our position. The company usually resists and the Department can either back up our position or go against it. This give and take usually results in a lower rate than the one requested. As the data on Lara’s rate approvals shows, however, when Consumer Watchdog is not in the room, the companies usually get close to what they want.

The other type of intervenor compensation is for the development of regulations. Lara has already imposed the standard that if you don’t agree with me, I will not pay you, which is why Consumer Watchdog and Consumer Federation recently sued him. The new regulations codify his right to deny compensation if he does not agree with the information presented.

The draft regulations stack the deck against intervenor compensation. In the hands of a vindictive commissioner like Lara, they could eviscerate the intervenor system and give insurance companies a free pass to rate hikes. The regulations are also likely to get Lara a corner office in an insurance consulting firm when he leaves office in 2027. If they go into effect, the rules could prevent the public from having representation in rate cases and the billions they have saved as a result.