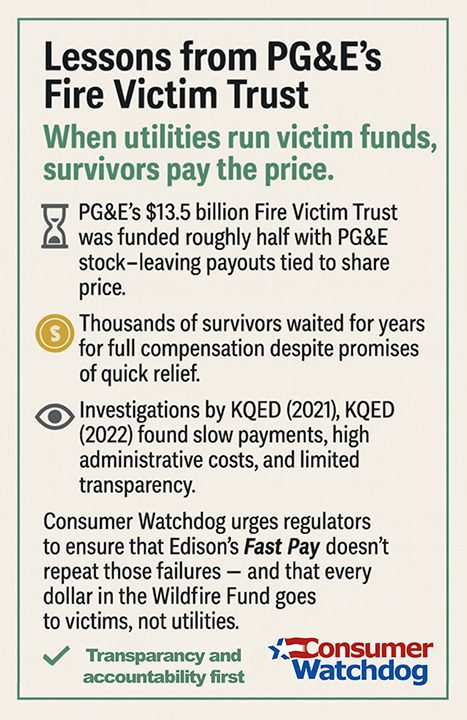

“Fast” Doesn’t Mean “Fair”

Southern California Edison (SCE) has announced a new “Fast Pay” program for Eaton Fire survivors. It promises quick cash from California’s Wildfire Fund — a fund paid for equally by ratepayers and utility shareholders to compensate victims when utilities spark catastrophic blazes.

But like most things labeled fast, Edison’s program may come at a steep price.

💰 What Fast Pay Offers — and What You Lose

- Non-negotiable offers. Edison decides what you get; you can’t bargain for more.

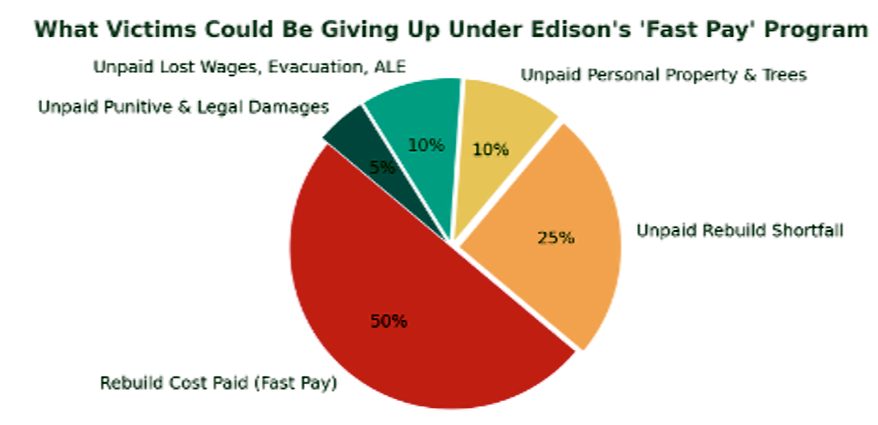

- Deep discounts. SCE’s examples show 54–73 percent shortfalls compared to actual rebuild costs — roughly a 50 percent discount overall.

- Missing categories. Fast Pay excludes or slashes compensation for trees and landscaping ($0), lost wages ($0), evacuation costs ($0), business losses (six-month cap), and punitive damages ($0)

- Insurance-offset trap. Edison automatically subtracts your insurance coverage — even if you haven’t received it. The fine print allows Edison to reduce payouts by the “total funds paid + 70 percent of unpaid” amounts.

That means survivors can be penalized for benefits they might never get, while still waiting on disputed insurance claims.

- Short deadlines. Claims close within three months, and reconsideration ends after nine months.

For many homeowners, that means giving up hundreds of thousands — even more than a million — dollars in exchange for a faster check that won’t rebuild their homes.

⚖️ Who Designed It — and Why It Matters

Edison hired Kenneth Feinberg, a nationally known mediator who has managed high-profile compensation funds such as the 9/11 Victim Compensation Fund, the BP Oil Spill Fund, and others.

Feinberg’s methods have drawn scrutiny in prior disasters:

- In 2011, U.S. District Judge Carl J. Barbier ordered Feinberg to disclose that he was being paid by BP when communicating with oil-spill victims and to stop implying that he was “neutral or independent.” In re Oil Spill by the Oil Rig “Deepwater Horizon,” MDL No. 2179, Rec. Doc. 912, Order & Reasons (E.D. La. Feb. 2, 2011) (Barbier, J.); New York Times, Feb. 2, 2011.

- Critics and some legal observers pressed Feinberg to be more transparent about his compensation and the fund’s methodology, particularly given the opacity of the Gulf Coast Claims Facility and its decision rules.

- In a DOJ-commissioned audit, the GCCF was found to have underpaid or denied valid claims, resulting in more than $64 million in additional payments to over 7,300 previously underpaid claimants. Some claimants were denied because they lacked documentation, though their losses may have been valid. (Gulf Coast Claims Facility Report of Findings & Observations, DOJ, 2012).

Edison has not disclosed how much it is paying Feinberg or what role he plays in structuring or approving Fast Pay offers.

Feinberg’s style emphasizes speed and simplicity — qualities that critics worry can shortchange victims who lack the resources to fully document losses. Survivors should use independent legal counsel and full disclosure before accepting any “fast-track” option.

(All references above are drawn from public court records and major news outlets. Consumer Watchdog expresses no opinion on Mr. Feinberg’s intent or conduct.)

🚫 Serious Questions About Legality

It is far from certain that Edison may lawfully use the Wildfire Fund in this way.

The Fund was created under AB 1054 (2019) to reimburse utilities after they pay eligible claims, subject to statutory oversight. It was not (on its face) designed to pre-fund discounted, nonnegotiable settlement offers to victims. If Edison uses the Fund as a front-end claims vehicle without oversight from the Catastrophe Response Council or proper review, it may exceed its legislative mandate.

Consumer Watchdog will monitor whether Fast Pay conforms to the letter and spirit of AB 1054 — and ensure ratepayer contributions serve victims, not utility liability minimization.

🕒 When “Fast” Might Make Sense

Some survivors — especially renters or those in urgent financial need — may decide that an immediate payment is the right choice. No one should be criticized for that. But every survivor deserves full, honest information before signing away rights.

Fast Pay can be right for a few, but it’s wrong for most homeowners who need to rebuild and recover their true losses. For most wildfire homeowners, the prudent approach is to compare Edison’s offer to your documented losses, insurance, and rebuild costs — before relinquishing your legal rights.

🔍 Before You Sign

- Consult an attorney experienced in wildfire law.

- Request a full, itemized breakdown of what is and isn’t covered.

- Compare Edison’s offer to your own rebuild and insurance numbers.

- Get it in writing. Once accepted, claims generally cannot be reopened.

💬 Don’t Be Burned Twice

Edison’s Fast Pay program risks turning a public safety fund into a utility liability shield. Victims deserve full compensation, not shortcuts that leave them shortchanged. Consumers shouldn’t have to trade fairness for speed.

Fast doesn’t mean fair.

Know your rights. Ask questions. Talk to a lawyer.